Summary

Our cost accounting experts created “The 10 Essentials of Cost Accounting Standards Compliance” that every company that holds contracts subject to Cost Accounting Standards must consider as they assess their compliance and risk profile.

Our team supports Government Contractors with navigating the complex Cost Accounting Standards requirements. This Cost Accounting Standards Summary provides insight into the process.

Cost Accounting Standards Requirements Summary Guide – 10 Essentials

The Cost Accounting Standards (CAS), CFR Title 48 Chapter 99, may present an onerous set of CAS requirements that apply to specific U.S. Government Contracts that dramatically impact your organization’s cost accounting practices and the disclosure of those practices.

If you are currently performing under flexibly priced and/or negotiated contracts, you may be subject to CAS. However, as you may not be aware, a significant number of these standards are also incorporated through the Federal Acquisition Regulation (FAR) Part 31 Cost Principles, even for contracts not subject to CAS. Contractors are often overwhelmed because the CAS requirements go beyond just the standards.

Further, the Cost Accounting Standards Board (CASB) has recently been active in reviewing certain standards for purposes of aligning the compliance requirements with those of traditional financial accounting and reporting, e.g., Generally Accepted Accounting Principles (GAAP). Contractors should remain aware of these CASB initiatives as changes to existing standards are likely to occur in

the future.

So why should contractors understand the CAS if they are subject to the standards or subject in part through FAR Part 31? Every contractor that holds CAS-covered contracts should ask themselves the following ten essential questions in our cost accounting standards summary.

Download Our Free CAS Compliance Guide

1) Do We Have A Complete List of CAS-Covered Contracts That Specifies The Type Of Coverage (full vs modified)?

It is critical for every contractor to have this information, as it is essential in meeting the requirements under FAR Part 30 Cost Accounting Standards Administration (more on this later). Many contractors have difficulties identifying their CAS covered contract universe and coverage type as they do not conduct timely, complete, and accurate contract briefs.

In addition, it is the Defense Contract Audit Agency’s (DCAA) expectation during the Accounting System Audit that there is a sufficient contract briefing process in place and that this information is readily available.

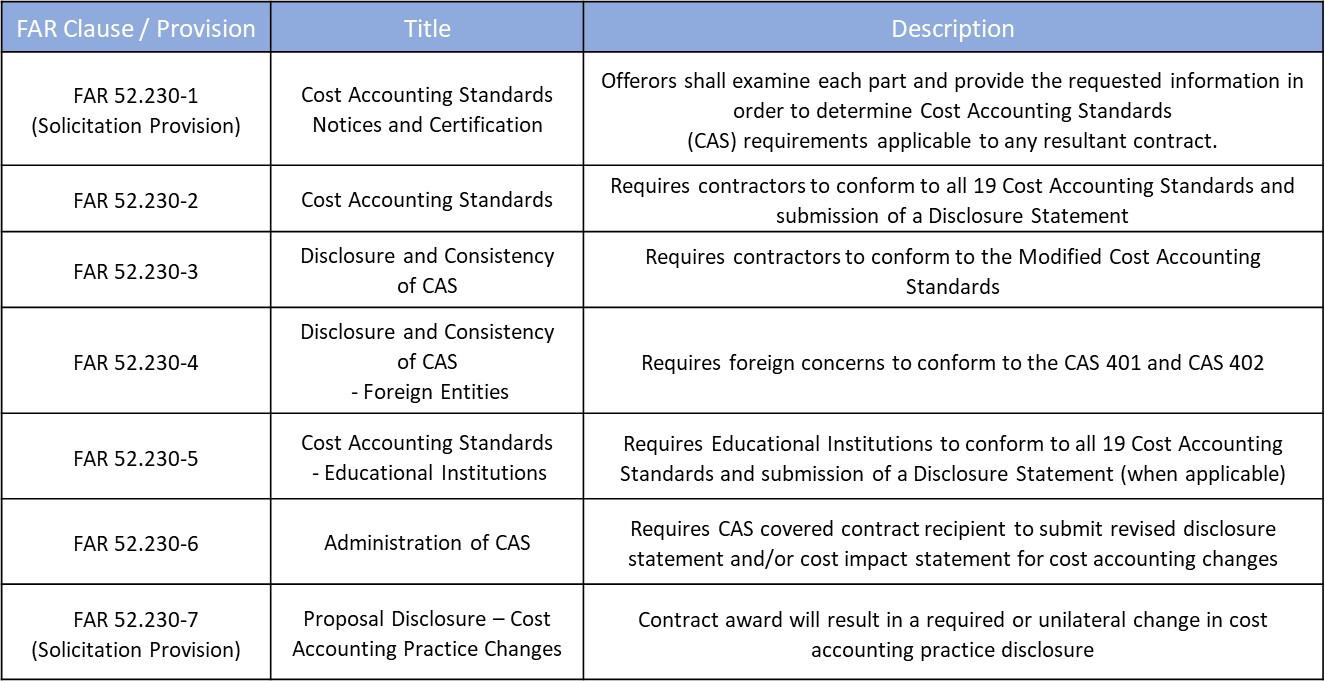

2) Are We Reviewing Solicitation Provisions and Contract Clauses Pertaining To The CAS And Do We Understand Their Implementations?

The table below summaries CAS-related provisions and clauses your organization should be aware of. If you think these clauses do not apply or sought an exemption, then negotiating the clause(s) out of the contract is paramount!

3) How Many Cost Accounting Standards Are There?

There are 19 standards that contractors need to conform to on contracts subject to full CAS coverage. The outline in our Free Download summarizes the standards grouped for your understanding. We recommend your organization have adequate resources and subject matter expertise to conform with all 19 standards (as applicable).

4) Do We Know When To File A CASB Disclosure Statement?

If you have a $50 Million trigger contract, it is easy to determine when to submit a disclosure statement. What about the Disclosure Statement applicability based on the look back requirement of CAS-covered awards received in the previous cost accounting period? How about the requirement for other segments that may not currently have any CAS-covered contracts but are included in the total price of a CAS-covered Contract? These can be trickier to navigate.

5) Is Our Disclosure Statement(s) Current, Adequate, and Inclusive of Only The Information Required To Disclose Our Cost Accounting Practices?

Your Disclosure Statement(s) must reflect your current cost accounting practices! Your organization should be aware of any cost accounting practice changes that have or will be implemented, and they must be properly reflected in the Disclosure Statement.

Furthermore, the Disclosure Statement is designed to define your cost accounting practices that pertain to how you measure, assign, and allocate cost. Information such as chart of accounts, department numbers, and policies and procedures (e.g., PTO benefits, description of accounting software, organizational charts, etc.) do not belong within the Disclosure Statement. These do not define your cost accounting practices!

6) Do We Know What Constitutes A Cost Accounting Change And What Does Not?

Cost accounting practice change(s) are a result of altering how you assign, measure, or allocate existing costs. Typical examples include changes in inventory costing methodology, grouping existing cost to a different indirect rate pool, changing the way you measure useful life of an asset, or changing the allocation base of an existing indirect cost pool.

Examples of situations that do not constitute a change to cost accounting practice include functions or activities created for the first time or eliminated, make or buy decisions, and changes in values of specific elements of an employee fringe benefits plan.

7) Do We Have A Process And Internal Controls Around Cost Accounting Practice Changes?

Your organization should have a defined process that ensures the right level of leadership is aware of the implications of making cost accounting practice changes and how this may affect your organization. What is advantageous for a particular proposal may be detrimental to the current CAS-covered contract population.

The process should also cover timely disclosures that could be driven from internally approved cost accounting practice changes and not to mention the 60 day notification “before implementation of the change” requirement under FAR 30.6 – CAS Administration

8) Are We Aware Of The Types of Cost Accounting Practice Changes And The Requirements Under FAR Part 30?

FAR Part 30 defines the types of cost accounting practice changes. Each change defined in our Free Download will have specific administration requirements and could impact CAS-covered contracts differently.

9) Do We Know How To Prepare And Submit A Cost Impact Proposal?

FAR Part 30 defines the process for submitting either a Rough Order Magnitude (ROM) or a Detailed Cost Impact and may be in any format acceptable to the CFAO. Additionally, a recent major defense contractor court case puts more emphasis on materiality and consideration on the cumulative impact to the U.S. Government when considering multiple cost accounting practice changes (i.e., “stacking”).

10) Do We Have A Process And Internal Controls Around Cost Accounting Practice Changes?

Many contractors have difficulties with CAS 402 – Consistency in Allocating Costs Incurred for the Same Purpose. Like costs in like circumstances, must always be treated consistently. The contract allowing (or not allowing) the cost to be billed as direct cost cannot define your cost accounting practice.

Does, “if the contract will pay for it, charge it direct” or “oh, we can’t bill that as direct cost, so stick it in overhead” sound familiar? These are common violations of CAS 402 and can have serious consequences for your organization.